When you start a business, there are endless decisions to make. Among the most important is how to structure your business. Why is it so significant? Because the structure you choose will affect how your business is taxed and the degree to which you (and other owners) can be held personally liable. Here’s an overview of the various structures.

When you start a business, there are endless decisions to make. Among the most important is how to structure your business. Why is it so significant? Because the structure you choose will affect how your business is taxed and the degree to which you (and other owners) can be held personally liable. Here’s an overview of the various structures.

Sole Proprietorship

This is a popular structure for single-owner businesses. No separate business entity is formed, although the business may have a name (often referred to as a DBA, short for “doing business as”). A sole proprietorship does not limit liability, but insurance may be purchased.

You report your business income and expenses on Schedule C, an attachment to your personal income tax return (Form 1040). Net earnings the business generates are subject to both self-employment taxes and income taxes. Sole proprietors may have employees but don’t take paychecks themselves.

Limited Liability Company

If you want protection for your personal assets in the event your business is sued, you might prefer a limited liability company (LLC). An LLC is a separate legal entity that can have one or more owners (called “members”). Usually, income is taxed to the owners individually, and earnings are subject to self-employment taxes.

Note: It’s not unusual for lenders to require a small LLC’s owners to personally guarantee any business loans.

Corporation

A corporation is a separate legal entity that can transact business in its own name and files corporate income tax returns. Like an LLC, a corporation can have one or more owners (shareholders). Shareholders generally are protected from personal liability but can be held responsible for repaying any business debts they’ve personally guaranteed.

If you make a “Subchapter S” election, shareholders will be taxed individually on their share of corporate income. This structure generally avoids federal income taxes at the corporate level.

Partnership

In certain respects, a partnership is similar to an LLC or an S corporation. However, partnerships must have at least one general partner who is personally liable for the partnership’s debts and obligations. Profits and losses are divided among the partners and taxed to them individually.

Call Newton Sankey & Co. today at 631-474-2500. We’ll set up a free consultation to discuss your new venture and how we can assist with our new business advisor and incorporation experience.

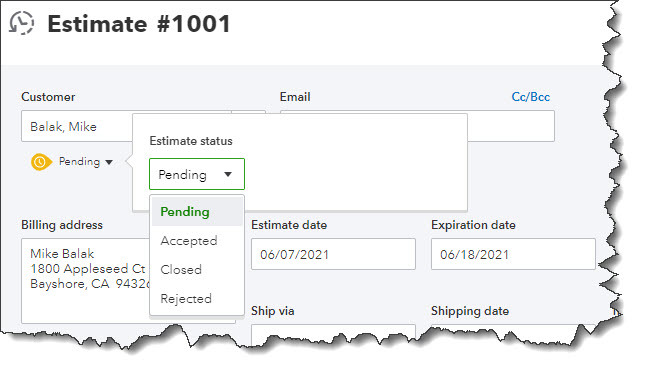

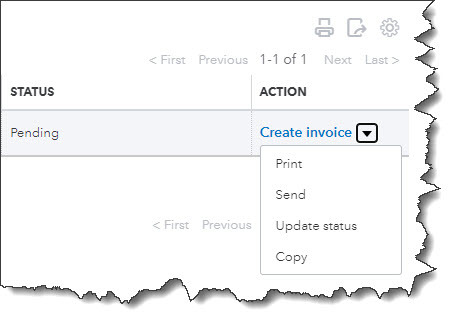

Whether you sell products or services, you may need to create estimates in QuickBooks Online. Here’s how it’s done.

Whether you sell products or services, you may need to create estimates in QuickBooks Online. Here’s how it’s done.

Incorporating your small business the right way can bring tax benefits and protect your personal assets. Read on to learn more about what incorporation is, why you might want to incorporate, and how an accountant can help you navigate the questions that come with selecting the right business structure.

Incorporating your small business the right way can bring tax benefits and protect your personal assets. Read on to learn more about what incorporation is, why you might want to incorporate, and how an accountant can help you navigate the questions that come with selecting the right business structure. …and tips on how to do it.

…and tips on how to do it. Paying employees seems easy enough. Their hours are logged, and you sign the checks; however, there’s more to payroll than that, and overlooking these critical aspects of paying your employees can have costly consequences. Here are five common payroll errors small business owners make and how to prevent them.

Paying employees seems easy enough. Their hours are logged, and you sign the checks; however, there’s more to payroll than that, and overlooking these critical aspects of paying your employees can have costly consequences. Here are five common payroll errors small business owners make and how to prevent them. New year, new challenges, and the potential for new successes. Here are five ways you can improve your financial management in 2021.

New year, new challenges, and the potential for new successes. Here are five ways you can improve your financial management in 2021.