While you may think it’s better to take care of your small business accounting tasks in-house, you may be surprised to know that your business can benefit from having a professional accountant or CPA handle the job for you. Here are the top three reasons to outsource your accounting.

While you may think it’s better to take care of your small business accounting tasks in-house, you may be surprised to know that your business can benefit from having a professional accountant or CPA handle the job for you. Here are the top three reasons to outsource your accounting.

1. Peace of Mind

The number one reason for outsourcing your accounting is the peace of mind you will get regarding managing your accounting records. A qualified accountant or CPA on your team allows you to gain access to their professional knowledge and experience. Further, you can even choose an accountant that specializes in your unique business needs. A professional can help you keep your business records accurate and up-to-date. For example, payroll and tax documents will be maintained appropriately and submitted promptly. Timely and accurate accounting reduces your risk of penalties resulting from inaccurate record-keeping or lack of knowledge regarding aspects of accounting like tax laws and deadlines.

2. Focus on Business Development

When you enlist the services of a qualified accountant or CPA to manage your small business accounting needs, you minimize the time that you or your senior staff must spend performing or micromanaging those tasks. Freeing up your time in those areas enhances your ability to maintain a keen focus on the day-to-day tasks your business faces and any additional business needs that arise. Being able to focus your time on managing and growing your business, you improve operational efficiency. As you develop strategic goals, you can convey those to your outsourced accountant to garner their professional guidance and support when executing and realizing those goals.

3. Save Money

Many small business owners feel that handling accounting tasks in-house is more cost-effective because they can utilize existing staff. However, consider the total cost involved in hiring or training a staff member to manage your business’s accounting needs. There is also the associated time expenditure related to supervising an employee who manages the accounting. For a dedicated in-house staff member to handle the task, you must consider the additional costs of payroll, payroll taxes, and employee benefits. There is also employee turnover to consider, which, if high, could lead to additional training and expenses. By not electing to have a full-time dedicated employee handle accounting in-house, you also save on space and technology required to accommodate that individual.

For these reasons – and more such as getting timely financial advice, understanding cash flow, and maximizing your tax savings opportunities – it’s time to outsource your business’s accounting needs. What you gain far outweighs the cost.

Contact our firm to find out how we can create a package of accounting services for your small business.

If you’re self-employed, understanding what’s deductible and recording all of your business expenses should be priorities.

If you’re self-employed, understanding what’s deductible and recording all of your business expenses should be priorities.

When you start a business, there are endless decisions to make. Among the most important is how to structure your business. Why is it so significant? Because the structure you choose will affect how your business is taxed and the degree to which you (and other owners) can be held personally liable. Here’s an overview of the various structures.

When you start a business, there are endless decisions to make. Among the most important is how to structure your business. Why is it so significant? Because the structure you choose will affect how your business is taxed and the degree to which you (and other owners) can be held personally liable. Here’s an overview of the various structures. Whether you sell products or services, you may need to create estimates in QuickBooks Online. Here’s how it’s done.

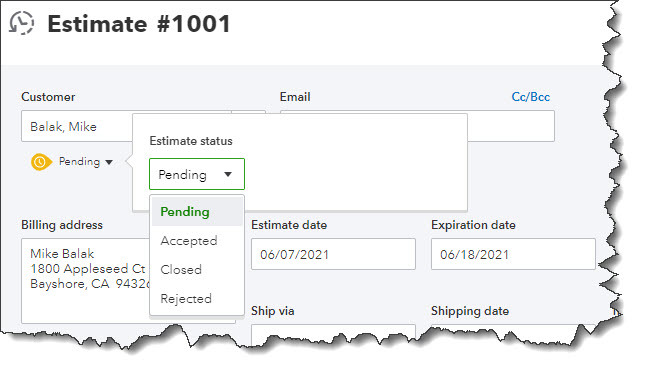

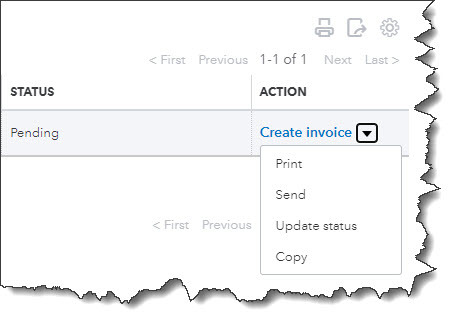

Whether you sell products or services, you may need to create estimates in QuickBooks Online. Here’s how it’s done.

Incorporating your small business the right way can bring tax benefits and protect your personal assets. Read on to learn more about what incorporation is, why you might want to incorporate, and how an accountant can help you navigate the questions that come with selecting the right business structure.

Incorporating your small business the right way can bring tax benefits and protect your personal assets. Read on to learn more about what incorporation is, why you might want to incorporate, and how an accountant can help you navigate the questions that come with selecting the right business structure. …and tips on how to do it.

…and tips on how to do it.